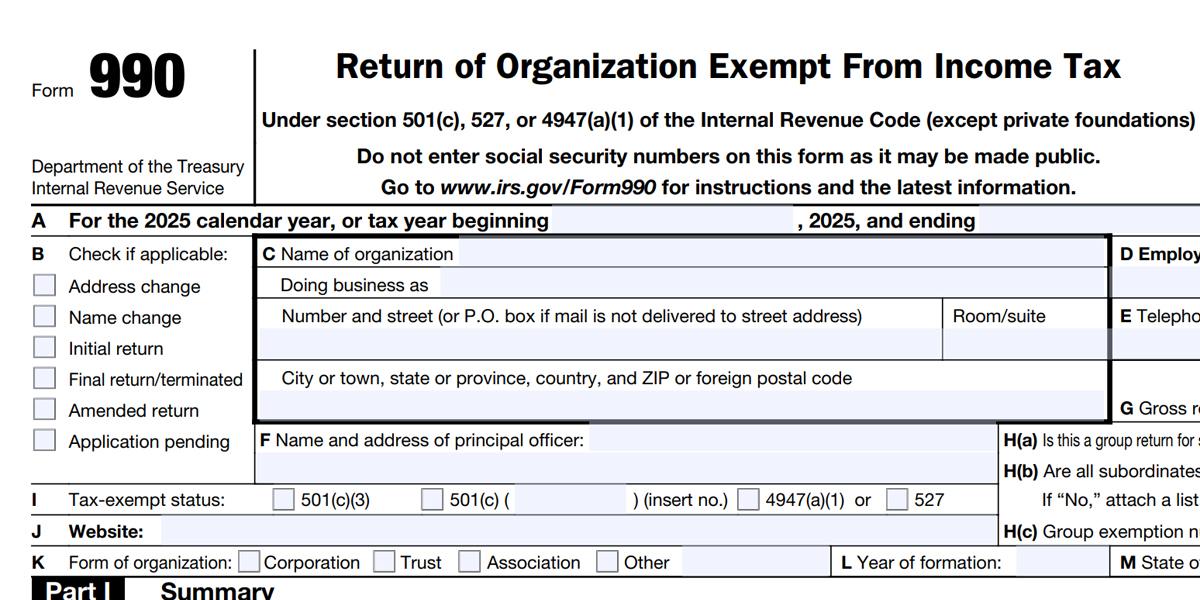

(image from https://www.irs.gov/pub/irs-pdf/f990.pdf)

The long-rumored reworking for the federal Form 990 has formally begun. The U.S. Department of the Treasury (DoT) announced that the Internal Revenue Service (IRS) plans to revise the Form 990 in an attempt to improve transparency, strengthen tax administration, and provide clearer reporting on certain activities of tax-exempt organizations described in section 501(c)(3) of the Internal Revenue Code.

There will be a special focus on government contracts, government grants, and fiscal sponsorship arrangements. The changes are intended to detect misconduct and hold wrongdoers accountable, according to a statement from the DoT.

When it comes to government contracts and grants, nonprofits might be required to provide clearer reporting on the sources and specific uses of public funds, although a definition of clearer was not described.

Fiscal sponsorship is an umbrella term for several longstanding and lawful structures through which a tax-exempt organization support charitable projects and initiatives.

According to the DoT announcement, “recent congressional oversight has raised concerns that some fiscal sponsorship arrangements may be used to obscure who is operating a project, who controls project funds, and how those funds are being used. Increased reporting can help address those concerns and make it harder for rogue organizations to hide behind opaque arrangements.”

New requirements might force nonprofits to identify sponsored projects directly, disclose who controls those funds, and how those funds are used.

“Public money and tax-exempt status demand public accountability,” Treasury Secretary Scott Bessent said via a statement. “We are ending the days of hiding fraud, abuse, and extremist activity behind complicated nonprofit arrangements. When bad actors misuse charitable structures, directors and officers should understand that transparency can lead to scrutiny, accountability, and liability under the law.”

Treasury and the IRS expect to publish proposed regulations and provide an opportunity for public comment before any reporting changes are finalized. Treasury and the IRS will consider administrative feasibility, proportionality, and reporting burden as the proposal is developed, according to the announcement.

“Tax-exempt status is not immunity from scrutiny,” Treasury Assistant Secretary and Acting IRS Chief Counsel Ken Kies said via a statement. “If an organization receives public funds or tax-deductible donations, it should be prepared to show who controls the money and where it goes.”